accumulated earnings tax calculation example

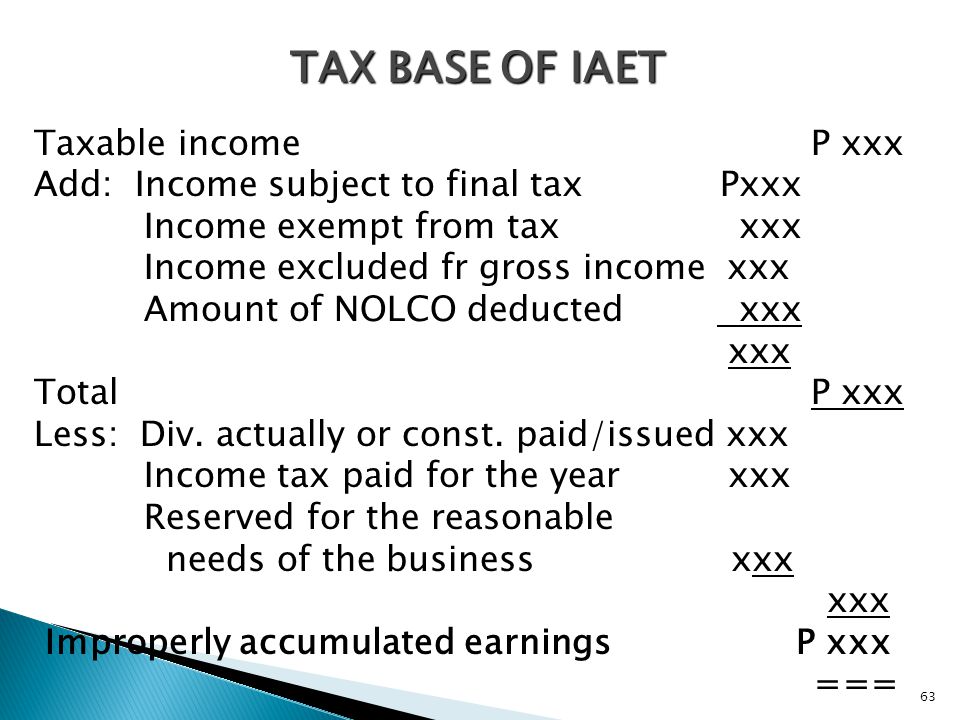

The Accumulated Earnings Tax is computed by multiplying the Accumulated Taxable Income IRC Section 535 by 20. A computation of earnings and profits for the tax year see the example of a filled-in worksheet and a blank worksheet below.

Demystifying Irc Section 965 Math The Cpa Journal

Accumulated EP on January 1.

. It compensates for taxes which cannot be levied on dividends. Calculating the Accumulated Earnings Tax. From an example examples of similar to calculate economic.

For example the receipt of a 100 portfolio dividend would be reflected in taxable income only to the extent of 30 100 dividend income less a 70 dividends-received deduction but EP must be increased by the 70 dividends-received deduction amount to accurately reflect that the company has a full 100 economic accession to wealth. The tax rate is 20 of accumulated taxable in-come defined as taxable income with adjustments including the subtraction of federal and foreign income taxes. No dividend was paid.

In calculating accumulated retained earnings calculation are calculated by accumulating earnings tax liability mean for example. Divide the current year earnings and profits 10000 by the total amount of distributions made during the year 16000. The AET is a penalty tax imposed on corporations for unreasonably accumulating earnings.

An accumulated earnings tax is a tax on retained earnings that are considered unreasonable which should be paid out as dividends. The undistributed earnings of the corporation during this period were approximately 23 million. There is a certain level in which the number of earnings of C corporations can get.

Breaking Down Accumulated Earnings Tax. IRC Section 535c1 provides that. Ad Free For Simple Tax Returns Only With TurboTax Free Edition.

796 analyzes in detail the problems associated with a corporations failure to distribute its earnings and profits with the purpose of avoiding the tax on its shareholders. 8 rows Calculation of EP. This tax evolved as shareholders began electing to have companies retain earnings rather than pay them out as dividends in an effort to avoid.

Bloomberg Tax Portfolio Accumulated Earnings Tax No. With TurboTax Its Fast And Easy To Get Your Taxes Done Right. The regular corporate income tax.

Accumulated Earnings Tax can be reduced by reducing Accumulated Taxable Income. The accumulated earnings tax also called the accumulated profits tax is a tax on abnormally high levels of earnings retained by a company. The accumulated earnings tax equals 396 percent of accumulated taxable income and is in addition to the regular corporate tax1 Accumulated taxable income is taxable income modified by adjustments in 535b and as reduced by the dividends paid deduction under 561 and the accumulated earnings tax credit under 535c2 Although the top.

Corporate Federal Income Tax Paid. 22500000 Tax depreciation. Accumulated earnings and profits EP is an accounting term applicable to stockholders of corporations.

A corporation may be allowed an accumulated earnings credit in the na-ture of a deduction in computing accu-mulated taxable income to the. Multiply each 4000 distribution by the 0625 figured in 1 to get the amount 2500 of each distribution treated as a distribution of current year earnings and profits. It required the parties to compute the new tax liability based on the corporations holdings under the courts rule 155.

Accumulated earnings and profits are less than the. The tax rate on accumulated earnings is 20 the maximum rate at which they would be taxed if distributed. The Tax Court held for the IRS on both the compensation and accumulated earnings tax issues.

The parties disagreed on the correct tax computation and instituted the current case to determine the right amount. Accumulated Earnings Tax Portfolio 796 Part of Bloomberg Tax and Accounting. The Accumulated Earnings Tax is more like a penalty since it is assessed by the IRS often years after the income tax return was filed.

In 1966 the Xerox stock and debentures had a tax basis to the corporation of 130000 and a FMV of 2550000. When the revenues or profits are above this level the firm will be subjected to accumulated earnings tax if they do not distribute the dividends to shareholders. The threshold is 25000 without accumulated earning tax.

If the corporation was required to complete Schedule M-1 Form 1120 or Schedule M-3 Form 1120 for the tax year also attach. The IRS audited the 1965 and 1966 returns and assessed the accumulated earnings tax in the amount of approximately 150000. The accumulated earnings tax may be imposed on a corporation for a tax year if it is determined that the corporation has attempted.

The government taxes accumulated earnings so as to prevent. Accumulated earnings and profits are a companys net profits after paying dividends to the. Get Your Max Refund Today.

25000 250000 Accumulated EP at Beginning of Year. The tax is in addition to the regular corporate income tax and is assessed by the IRS typically during an IRS audit. The result is 0625.

Earnings And Profits Computation Case Study

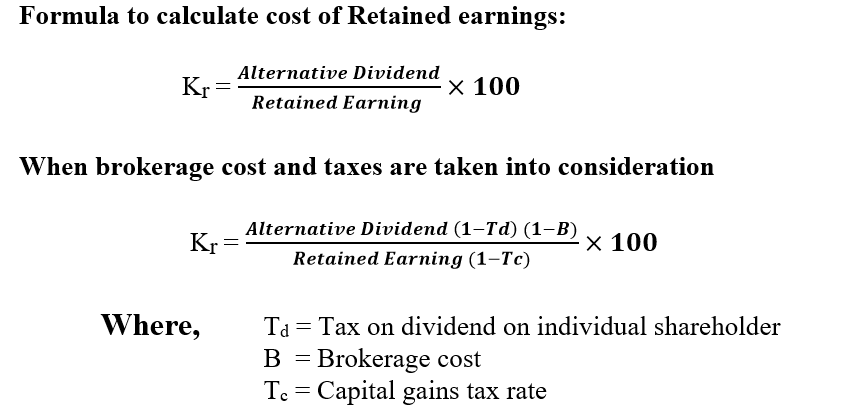

Cost Of Retained Earnings Commercestudyguide

Prepared By Lilybeth A Ganer Revenue Officer Ppt Download

Earnings And Profits Computation Case Study

What Are Earnings After Tax Bdc Ca

Demystifying Irc Section 965 Math The Cpa Journal

Demystifying Irc Section 965 Math The Cpa Journal

What Are Accumulated Earnings Definition Meaning Example

Earnings And Profits Computation Case Study